PerformLine monitors thousands of pieces of published content daily for compliance using proprietary technology and expert rulebooks to look for potential violations.

This study was conducted over a 6-month period reviewing thousands of web pages and social media posts for personal loan offerings.

Here are the top four remediated terms and categories that companies use to ensure that loan products are being promoted accurately across known (and unknown) places across the web and social media.

#1 - PAYDAY

The top most remediated compliance term for personal loans is “payday.”

In this context, we’ve seen instances where external entities use brand names to falsely promote certain products or services as “payday” loans, quick cash, instant money, etc. and encourage consumers to apply for a loan. The consumer thinks they’re applying for a product from a certain company, but instead, they’re giving their information to a fraudulent third party that has no relation to the brand that they are promoting.

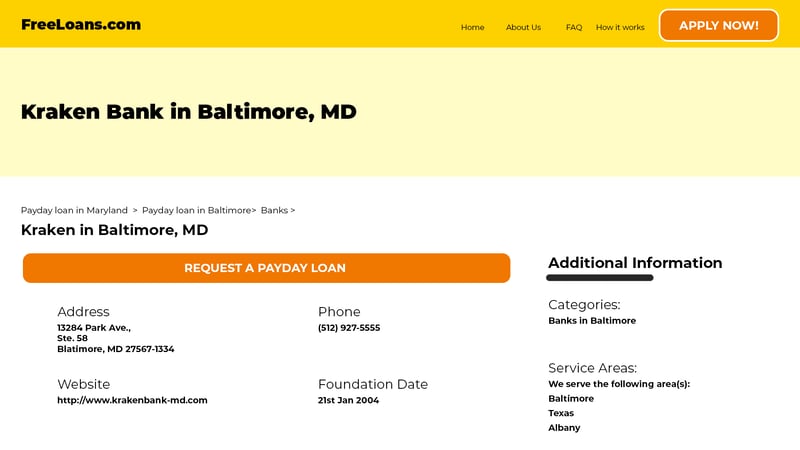

In this example, the call-to-action “request a payday loan” does not bring the consumer to the company’s website.

A company is responsible for monitoring all places in which its brand is being promoted (both known and unknown), whether or not third parties are involved.